Borrowers have become accustomed to instant access. They can order products online, transfer money between accounts, and receive payments within seconds. As these expectations continue to shape consumer behavior, they are increasingly influencing the lending industry as well.

When a loan is approved, borrowers no longer compare their experience solely against other lenders. They compare it against every other digital experience in their lives. Waiting days for funds to arrive can feel outdated, particularly when the need for funds is urgent.

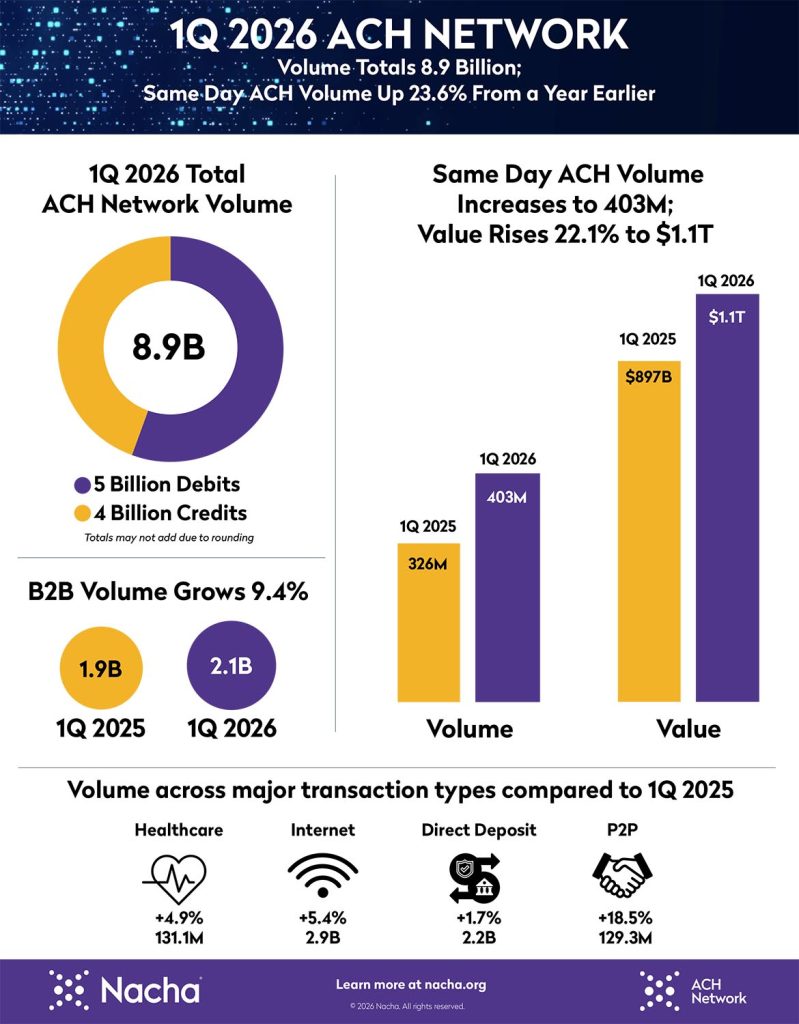

Recent ACH Network growth data suggests that financial institutions and businesses are responding to this demand for faster payments. During the first quarter of 2026, Same Day ACH volume increased 23.6% year-over-year to 403 million payments, while the value of those payments reached $1.1 trillion, an increase of 22.1%.

These numbers demonstrate that faster payment capabilities are becoming increasingly important across the financial ecosystem, including lending.

Same Day ACH volume reached 403 million payments during the first quarter of 2026, while payment value exceeded $1.1 trillion for the second consecutive quarter.

Why Faster Funding Matters

For many borrowers, access to funds is the most important part of the lending experience.

A streamlined application process and quick approval lose much of their value if borrowers must wait days to receive their money. Whether funding is needed for emergency expenses, home repairs, vehicle repairs, medical bills, or short-term cash flow needs, delays can negatively impact borrower satisfaction.

Faster funding can help lenders:

- Improve borrower satisfaction

- Increase repeat borrowing activity

- Strengthen customer retention

- Differentiate themselves in a competitive market

- Reduce funding-related support inquiries

As borrower expectations continue to evolve, funding speed has become an important part of the overall customer experience.

Same Day ACH Remains a Practical Funding Solution

While much attention has been focused on real-time payment networks such as RTP and FedNow, Same Day ACH continues to experience significant growth.

One reason is accessibility.

Most financial institutions already participate in the ACH Network, making Same Day ACH a practical option for many lenders that want to accelerate funding without implementing entirely new payment workflows.

Same Day ACH can help lenders:

- Deliver funds faster than traditional ACH

- Improve operational efficiency

- Reduce delays caused by batch processing

- Provide more predictable settlement timing

- Expand funding options for borrowers

For many lending organizations, Same Day ACH serves as an effective bridge between traditional ACH processing and real-time payment solutions.

ACH Continues to Support Digital Lending Growth

The first-quarter ACH data also showed strong growth in business-to-business payments and continued expansion across internet-based transactions.

This broader growth reflects an ongoing migration away from paper-based payment methods and toward digital payment experiences.

For lenders, this trend extends beyond loan funding. ACH remains a critical tool for:

- Recurring loan payments

- Account verification processes

- Consumer disbursements

- Collections and repayment programs

- Settlement and reconciliation operations

As lending becomes increasingly digital, ACH continues to provide the foundation for many borrower-facing payment experiences.

What Lenders Should Do Now

The continued growth of Same Day ACH provides an opportunity for lenders to evaluate whether their payment strategy aligns with borrower expectations.

Consider the following questions:

- How quickly can borrowers receive funds after approval?

- Are funding delays creating friction in the borrower experience?

- Could Same Day ACH improve customer satisfaction or retention?

- Are there opportunities to incorporate RTP or FedNow alongside existing ACH processes?

Lenders that proactively evaluate their payment capabilities today will be better positioned to meet the expectations of tomorrow’s borrowers.

Final Thoughts

The first quarter of 2026 highlighted the continued strength of the ACH Network, but the most significant takeaway for lenders may be the ongoing growth of Same Day ACH.

As borrowers increasingly expect faster access to funds, lenders must balance speed, efficiency, risk management, and operational simplicity. Same Day ACH continues to provide a practical solution that helps bridge those competing priorities.

At Viking, solutions such as VIKExpress, VIKEdge, and VIKEngage help lenders modernize payment operations, improve funding experiences, and maintain visibility into transaction performance as payment expectations continue to evolve.

May 7, 2026

About John O’Shea

He is a former founder and owner of Triad Financial Services and has served in similar roles at GMAC/Residential Funding, AllianceOne and ICT Group (now Sykes). He has performed for 28 years as a senior executive in the ARM, Customer Contact and BPO markets. He is a graduate of St. Olaf College.